But Hexaware Technologies’ February 19 listing was like a party. The moment the 33-year-old, Mumbai headquartered company’s stock started trading on the bourses, the celebratory mood at the bell-ringing ceremony was unmistakable.

Unlike the usual quiet corporate gatherings, Hexaware’s leadership, employees, and investors made it a grand affair—more like a millennial after-party than a solemn listing event.

And why not? For a company that has transformed itself over the last decade, consistently delivering double digit revenue growth, returning to the public markets after delisting in 2020 was a milestone that symbolized its evolution from a lower-tier IT firm to a fast-growing contender aiming for the big league.

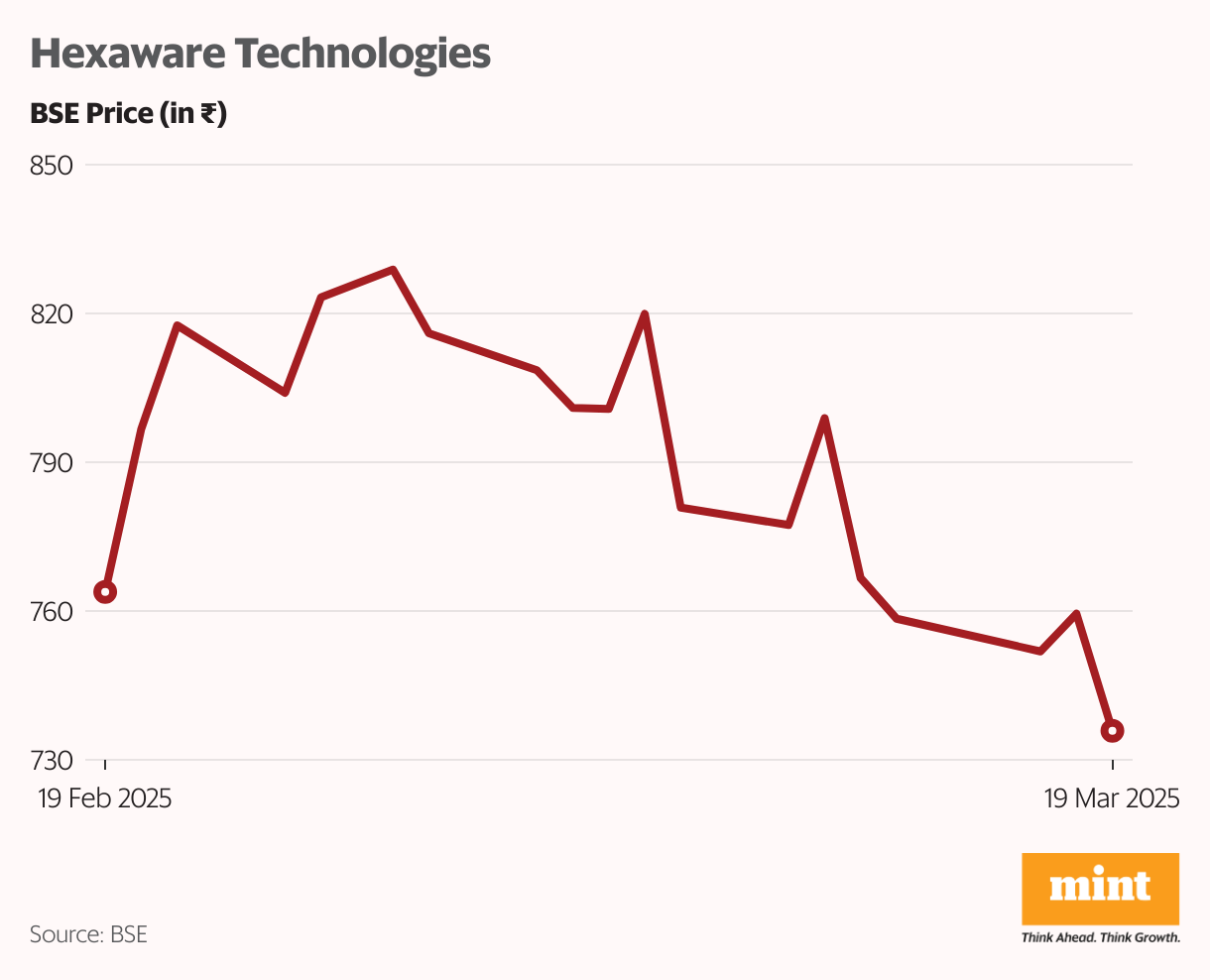

However, just weeks after the euphoria, the reality of market scrutiny hit hard. $1.43 billion Hexaware’s first post-IPO quarterly results (the company follows a January-December financial year) on 7 March failed to impress investors, and the stock took a beating. The stock declined 6.75% to hit an intra-day low of ₹764 on the NSE. On 19 March, Hexaware closed at ₹736 on the BSE, down 3.09% from its previous close.

But CEO R. Srikrishna is unfazed. “Our numbers were very good. I know the market didn’t like it, but it’s going to take some time to educate it on our cyclicality,” he said.

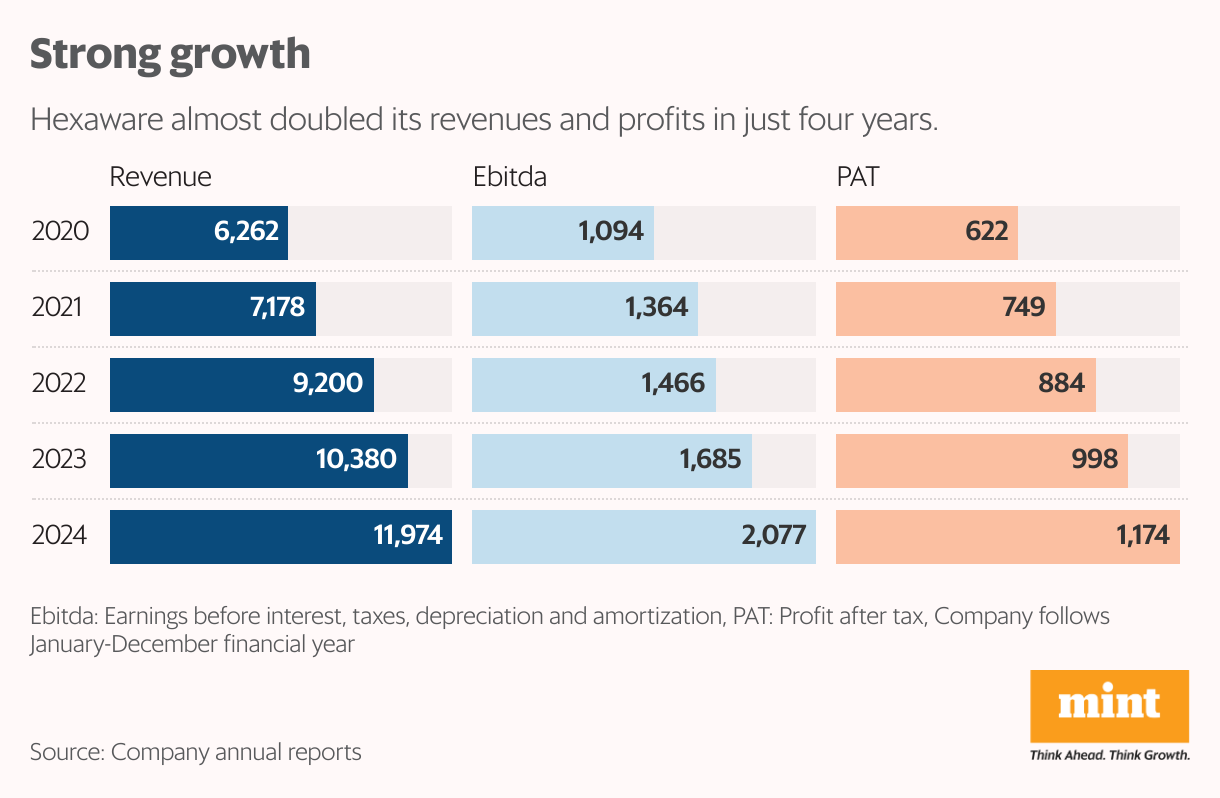

The company posted 18.5% y-o-y growth in revenue, with Ebitda ( surging 48% and PAT (profit after tax) shooting up 65% (compared to Q4, 2023). “It’s hard to have a better set of numbers than this,” added Srikrishna, popularly called Keech, a nickname he got in school back in the early 1980s, from a Tamil film character with the same name.

While Keech has a sanguine view, the market was disappointed because Hexaware’s sequential revenue growth in constant currency terms was just 0.2% y-o-y, raising concerns over near-term demand. Moreover, the management commentary on the challenging macro environment raised concerns about the growth outlook, leading to the stock taking a beating.

“The macros got somewhat worse in the last two weeks (due to inward-looking US policies). But our performance will be resilient to that,” said Keech.

That optimism is because the company does not have exposure to tariff-impacted sectors such as metals, oil, automobiles, food and agriculture. “But it (tariffs) impacts consumer sentiment, which could mean delays as customers adjust to some of the new tariff arrangements,” said the Hexaware CEO.

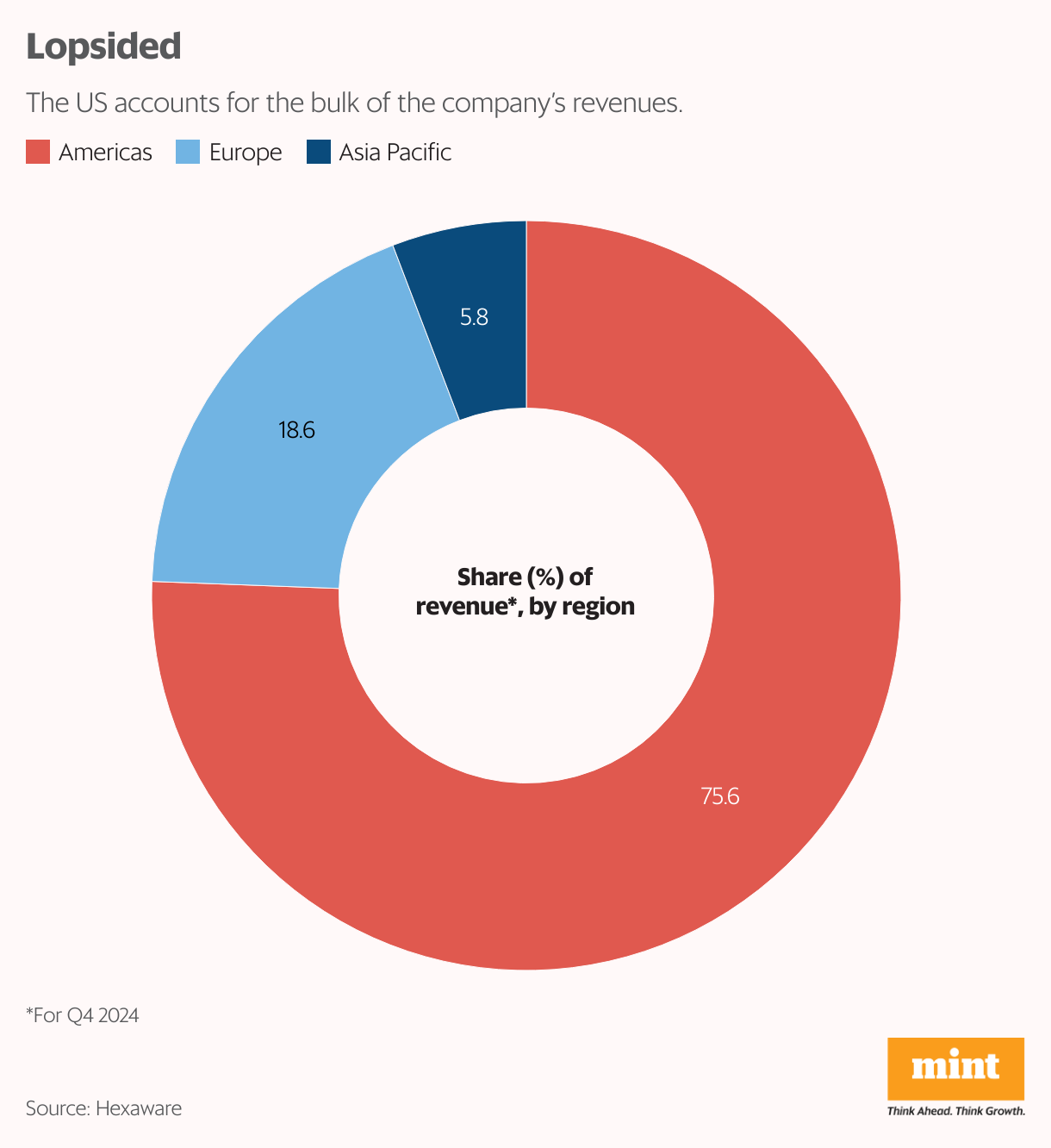

Keech is confident that Hexaware will stay resilient and deliver in 2025 as well. The company gets 73.4% of its business from the US market, 22% from Europe and the rest from the Asia Pacific region.

Hexaware has one $100 million client and over 125 accounts generating $1-5 million in revenue.

While seasonality impacts Q4 and Q1 performance, the company’s stronghold in BFSI, healthcare, and the accelerating momentum in the technology sector position it well for sustained growth,” said Praveen Bhadada, CEO & founder of Neovay Global, an advisory firm.

Hitting its stride

Hexaware was founded by entrepreneur Atul Nishar back in 1992 as Aptech Information Systems. At the time the company focused on computer graphics and animation training. Later it expanded to a broader services spectrum that included enterprise application integration and application management for global clients. Nishar was chairman of IT body Nasscom in 2000.

In 1997, the company changed its name to Aptech and was rechristened again as Hexaware Technologies in 2002, just after going public in 2001. In 2003 Nishar sold the computer training business to Chennai-based education software company SSI.

An old horse, Hexaware has seen the rise of IT sourcing, the Y2K opportunity and more. Yet, unlike Indian IT majors TCS, Infosys, HCL and Wipro, which rode the global IT outsourcing boom of the 1990s and 2000s, it remained a relatively niche player.

It wasn’t until 2013, when Baring Asia Private Equity (now called EQT Private Capital Asia) acquired a majority stake, that the company started scripting a new growth story. That year, Nishar exited the company he founded but remained as a director until November 2021.

The decision to delist in 2020 was taken by Baring as part of its exit strategy. Hexaware re-listed last month.

When Keech, who was hired from HCL, took over as CEO in 2014, Hexaware was a $380 million company. By 2024, it had grown nearly 4x to $1.43 billion in revenue.

Hexaware has scaled up significantly in the last decade, albeit on a small base. It is still 20x smaller than leader TCS and 8x smaller than HCLTech, which is also part of the top four IT services companies.

Hexaware is still 20x smaller than leader TCS and 8x smaller than HCLTech.

The transformation was systematic. The company expanded its delivery footprint from being largely India-centric to adding centres in the Philippines, Argentina, and Eastern Europe. Hexaware diversified its portfolio, focusing on three core services: software engineering, technology operations, and AI/data analytics. This helped it move up the value chain, secure larger deals and more strategic partnerships.

In the last decade, which saw private equity and Keech coming in, Hexaware has consistently delivered double digit growth.

PE: The growth enabler

Unlike some of its peers, which grew organically, Hexaware’s growth was driven by its private equity backing. Baring Asia played a pivotal role in its turnaround, providing the strategic direction and focus needed for accelerated growth.

In 2021, US-based Carlyle Group acquired Hexaware from Baring, further strengthening its global ambitions.

According to Gaurav Vasu, CEO of UnearthInsight, a Bengaluru-based analyst firm, private equity backing gives firms like Hexaware an edge in financial discipline and M&A strategies. “PE-backed firms tend to grow faster and use acquisitions more effectively. They follow a structured playbook, which has worked well for Hexaware,” he noted.

Coforge, another small firm that started in the 1990s and delivered a breakout performance only in recent years, was backed by Baring Asia. It was earlier known as NIIT Technologies.

Unlike some of its peers, which grew organically, Hexaware’s growth was driven by its private equity backing.

However, Keech differs on the role of PE. “The change was not just because of the ownership change. It’s because of the leadership team, which identified opportunities and steered Hexaware on the growth path.”

Keech attributes Hexaware’s success to a fundamental shift in strategy. “We were best known for implementing PeopleSoft back then. Today, that’s just 2% of our revenues. We’ve completely transformed in terms of leadership, capabilities, and client focus,” he said. PeopleSoft provides a suite of applications in HR, customer relationship management, supply chain management, and so on.

In the decade prior to Keech’s joining, the industry grew 6x while Hexaware grew less than 3x. “The premise in the industry back then was that smaller companies would continue to grow slower and that they can’t compete with the larger players. We flipped that. We changed growth rates in multiple years,” said Keech.

The change was not just because of the ownership change. It’s because of the leadership team, which identified opportunities and steered Hexaware on the growth path

– R. Srikrishna

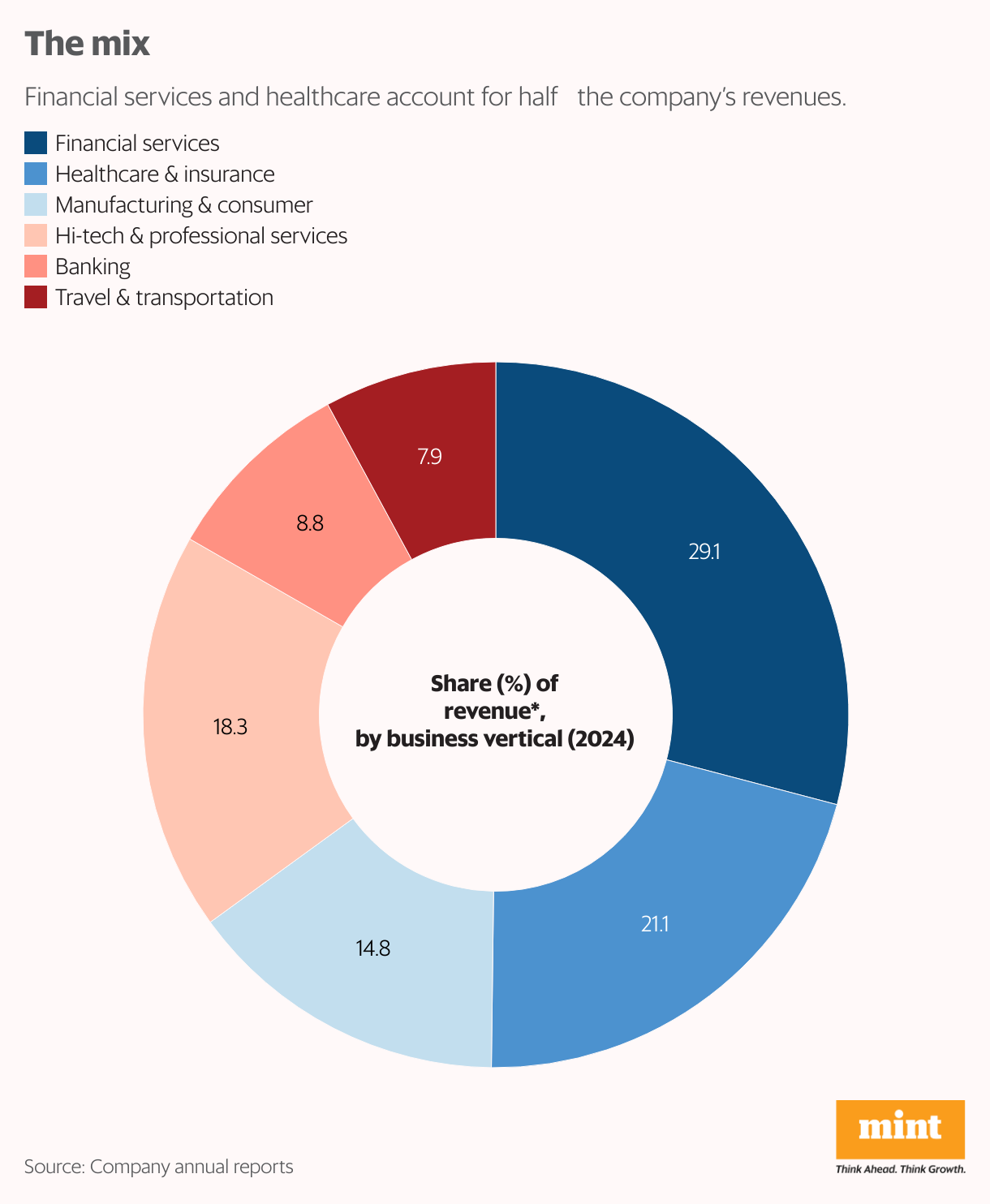

The company’s healthcare and life sciences vertical has seen a CAGR (compounded annual growth rate) of 22% in the last five years, BFSI, with a focus more on insurance, grew at a CAGR of 20% and so did manufacturing and hi-tech.

In 2024, financial services was the largest vertical, with a 29.1% share of the business. Healthcare & insurance was the second largest, accounting for 21.1% of the revenue, followed by the high-tech and professional services vertical, with an 18.3% share.

Hexaware wants to more than double its business to $3 billion in the coming years. “To me, the timeline is going to be between 2028 and 2030. In the case of the latter, it will require a CAGR of 13-14% and the former, 20%,” said Keech.

To get to the goal by 2028 will require strategic acquisitions as well. Potential M&A targets include companies specializing in security, data analytics, product engineering, cloud solutions (especially Microsoft Fabric, a data analytics platform) and those offering delivery capabilities in Latin America and Eastern Europe. Hexaware has also doubled down on hyperscale partnerships with (large cloud services providers) AWS, Azure, and Google Cloud, which can help drive revenue growth.

However, Neovay Global’s Bhadada pointed out that Hexaware will need to improve its effective billing rates and employee realization. “Revenue per employee remains lower than its peers. Increasing offshore business can be a crucial lever for cost efficiency and margin expansion,” he said.

Hexaware has 32,000 employees for $1.4 billion revenue, while Coforge had $1.6 billion for a 33,000 headcount and Persistent Systems 23,000 employees for $1.1 billion revenue. Tasks around AI could help improve billing rates and revenue per employee.

AI and automation

With AI reshaping enterprise IT, Hexaware is betting big on GenAI-driven solutions. The company has integrated AI into its core platforms, RapidX, Tensai, and Amaze. Tensai, an automation platform, for instance, now includes more than a dozen AI-powered modules that enhance tech outsourcing.

RapidX is actually built on GenAI and used for cloud, business process automation and data management. In Amaze, a cloud transformation platform, there are some components that use GenAI. “Every software development project we do will now have an AI component,” Keech said. “Instead of selling AI as standalone projects, we are embedding it into our core services.”

This platformization is helping Hexaware bolt on AI across services. “AI isn’t about doing proof-of-concept projects. It’s about embedding AI into everyday enterprise functions. That’s where we see a sustained revenue impact,” Keech added. For example, using conversational AI, Hexaware helped one of its banking customers cut contact centre costs by 25%. In another instance, Hexaware helped a food delivery app get a 136% surge in traffic after using personalized AI engagement.

Taking on the big boys

Despite its breakout growth, Hexaware still operates in the shadow of giants like TCS, Infosys, and Wipro. But Keech argues that the competition isn’t just from the likes of Coforge and Persistent. Instead, he said , Hexaware regularly competes with large IT companies for major client accounts.

“Most large global customers work with five partners—usually three large IT firms, one mid-tier challenger like us, and a niche player,” Keech said. “That means our day-to-day competition is with the big players.” Often, global companies use multiple tech services vendors to access specialist skills and mitigate the risks of depending on only one vendor.

This is both an opportunity and a challenge. Hexaware’s diversification strategy has helped—it derives revenue from BFSI, healthcare, as well as mid-sized travel and transportation and high-tech clients rather than over-relying on one or two segments.

The top 10-20 clients have remained with Hexaware for 12-15 years.

Keech himself is deeply involved in sales. “He’ll take a flight at a moment’s notice to meet clients and close deals. To his credit he has also created a flat structure, which brings a sense of belonging among employees. This was also very visible at the re-listing ceremony,” said an industry watcher, who did not want to be named.

Ramkumar Ramamoorthy, partner at Catalincs, a growth advisory firm and former CMD of Cognizant India, added that the CEO’s “hands-on leadership style has been key to Hexaware’s transformation. Keech is among the best sales-oriented CEOs in the industry”.

This client-centric culture has translated into strong customer stickiness. The top 10-20 clients have remained with Hexaware for 12-15 years. “That’s a rarity for mid-tier IT firms. In fact, it’s a hallmark of a well-run company,” said Ramkumar.

What next?

While Hexaware has defied expectations over the past decade, its next phase of growth won’t be easy. The leadership team that has transformed it from an also-ran into a force to reckon with may not be around in later years. It also faces greater scrutiny after becoming a public listed company once again.

Vasu added, “The pressures of public scrutiny and retaining talent will be critical. Hexaware must find its next set of sweet spots, whether in AI, new verticals, or strategic acquisitions.”

While it has the wind in its sails, the geopolitical environment and inward-looking policies in its biggest market, the US, will not be easy to navigate.

Also, it has limited ability to take part in larger deals compared to industry giants such as TCS or HCL because of revenue and other filters. Most large players today operate on every continent, whereas Hexaware is heavily dependent on the US and Europe for over 90% of its business.

Hexaware must find its next set of sweet spots, whether in AI, new verticals, or strategic acquisitions

– Gaurav Vasu

For now, Hexaware remains one of the fastest-growing small IT services firms. Whether it can sustain this growth trajectory and reach its $3 billion target will depend on the company’s ability to execute bold strategies while navigating the complex global IT landscape.